April 20, 2016

Investing 101

If You Want to Own Property, REITs Provide a Huge Head Start vs Direct Investment

By Victor Haghani 1

If you’ve decided you want to allocate some of your savings to real estate, you may want to compare the merits of publicly listed REITs, like Vanguard’s (VNQ), versus investing in buildings directly, through private investment partnerships.2 At Elm Partners, we use REIT ETFs, particularly Vanguard’s VNQ and VNQI, for US and non-US property exposure in our globally diversified portfolios.

The many individual benefits of REITs add up to a surprisingly big head start over private investment vehicles. While discerning private investors should be able to identify individual properties with higher returns than the average REIT-owned property, they need to generate returns about 4% higher just to catch up with the efficiencies of REITs. As detailed in the table below, this 4% comes from four main sources: higher costs, higher taxes, less diversification and lower liquidity of private investments. This 4% hurdle translates into an 8% hurdle for return on equity when the property investment is 50% leveraged with debt.3

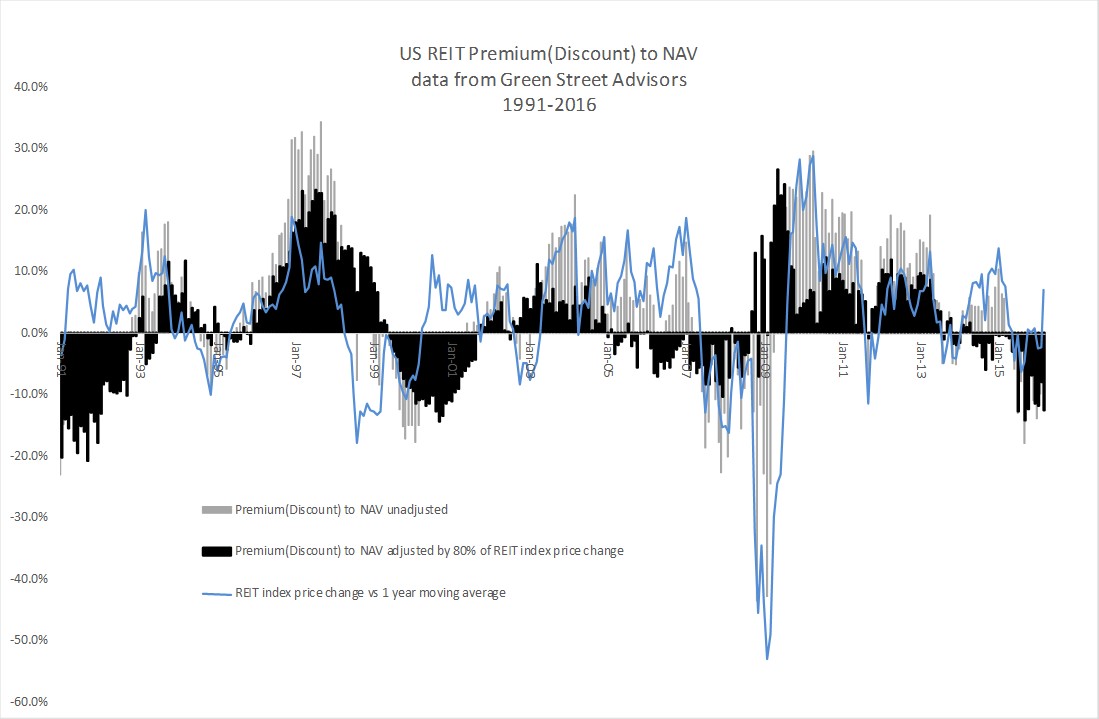

A major worry of REIT investors is that it’s impractical to analyae all the individual holdings, resulting in the risk of buying real estate at a substantial premium to fair value (NAV). Unfortunately, US REITs are not required to give an estimate of their NAV and so we have to rely on several specialist research companies to make those estimates. As you can see in the chart below, over the past 25 years REITs have averaged a 4% premium to NAV, within a wide range of a 45% discount in 2009 to a 35% premium in 1997. Given the enormity of the task of valuing thousands of properties without specific, inside details about each property, we shouldn’t expect these third party NAV estimates to be very accurate. Indeed, it appears that the divergences may be exaggerated by the NAV estimates lagging public market price moves. Making a simple adjustment for this lag reduces the volatility of the divergence from NAV by about 40%, and brings the average to a 1% premium, as shown by the black bars.

I didn’t list this as a cost or benefit of REITs vs private holdings, because, depending on timing, this could reduce or enhance returns. To flesh out a plausible negative scenario, let’s assume an investor bought REITs at a 10% premium and sold them 15 years later a 10% discount. That would cut the REIT head start of 4% a year down by only about 15%, in terms of the required return on the underlying unleveraged property investment. The return reduction could turn out to be even less than that, because when REITs trade at a premium to NAV, it is possible for them to add to their property portfolios by issuing shares to private sellers, and thus the premium to NAV can come down without harming returns.

I’d be remiss if I didn’t list any benefits of holding property directly. Some argue that illiquidity can be a blessing in disguise, forcing investors to hold for the long term. Ignorance of daily price fluctuations may make the private investing experience more blissful too. Indeed, it may be that many large fortunes have arisen from people feeling “locked” in to the companies they built or the properties they bought. Property investors also derive comfort and psychic value from the tangibility of their property investments, and the ability to touch and see their investments may make their investments feel less risky than more abstract and indirect holdings through REIT ETFs. Finally, while REITs may be the dominant structure for delivering passive real estate exposure, private capital may remain the preferred structure for certain activities such as development and aggregation, even if ultimately for sale to REITs.

The benefits of REITs are already well known. Investors have been enthusiastically voting for REITs with their investment dollars, bringing the value of REITs close to $1 trillion. REITs currently own about 1/8 of commercial real estate in the US, up from less than 1% in 1990.4 REITs are on track to own over 50% of all US commercial real estate by 2040 even if these trends slow down by half.

I hope this note has been helpful in cataloguing and attempting to quantify the relative merits of REIT vs private ownership, summing up to a 4% hurdle that privately owned properties need to exceed relative to REITs. In a future note, I’ll address the more fundamental question of the long-term expected return of real estate given today’s valuation levels.

Table: Comparison of REIT vs private real estate investing

| 0.7% | Avoiding transactions costs. Typically, when buying a building, an investor will incur about 5% as brokerage, legal, transfer tax and other fees, and loan arrangement fees of 2%, which together equate to about 0.6% pa over the 15 year investment horizon we assume throughout this analysis.5 When investing in a REIT, these costs have already been paid. |

| 0.5% | REITs typically have lower borrowing costs. I assume REITs can borrow about 1% more cheaply from banks than private borrowers on individual properties. |

| 0.9% | REITs generally benefit from lower management costs due to economies of scale, and lack of carried interest. This calculation assumes REITs have 0.5% lower management fees and no 15% carried interest. The cost savings can be much higher in the case of small properties managed by the investor, if the investor were to accurately bill himself for the value of his time. |

| 0.6% | Tax savings will vary depending on the characteristics of the investor and the site of the property. One benefit of ownership through a REIT is that income that is passed out as dividends are not subject to state (or city) tax, in most states. For high tax sites, like NY or CA, this can amount to a tax saving of 10% of income, assuming that the ultimate investor is in a low or no tax state. REITs allow for longer term holding than private investments, as the manager usually has an incentive to realize gains to be paid his incentive fee. A further potential saving is that private ownership structures usually throw off miscellaneous itemized deductions which many high rate US taxpayers cannot deduct.6 For non-US investors, the tax savings of REITs over direct investments might be 0.8% greater. 7 |

| 1.0% | Substantial diversification is provided by REIT ETFs, such as (IYR), (VNQ), (SCHH) and (RWR), which hold over 100 individual equity REITs. These REITs in turn provide ownership in thousands of properties in different locations and of different types, many of them large properties in prime locations that would be hard for most investors to access through private ownership. I estimate this effect perhaps over-simplistically by assuming a private portfolio will be 25% riskier than a diversified REIT ETF, and so the investor would need to get 25% more return for bearing that risk. |

| 0.5% | Liquidity: REITs are liquid. Private property takes time to transact, and the decisions to buy or sell may depend on the desires and personal circumstances of the manager of the property or other investors in the private deal. REITs are easily marginable, which allows investors to efficiently raise temporary liquidity. Listed options markets that have developed around REITs give investors even greater flexibility. An overview of the academic literature on pricing illiquidity by A Damodaran of NYU suggests a number much higher than 0.5%, but I am sympathetic to the notion that liquidity is valuable but over-priced by the market.8 |

| 4.2% | Total Head Start of REITs vs Private Ownership |

- Victor is the Founder and CIO of Elm Partners. Past returns are not indicative of future performance. This not is not an offer or solicitation to invest.

Thanks to Chip Parkhurst, who did much of the research for this note as a summer intern at Elm Partners, my friend Larry Hilibrand for invaluable help from start to finish, and my colleagues at Elm Partners.

- In this note, I am using the term REIT to refer to publicly traded equity Real Estate Investment Trusts in the US. There are other types of REITs and also there is a large and growing non-US REIT market.

- REITs are one of the most indexed of all market segments, with Vanguard, Blackrock and StateStreet owning about 30% of the large REITs, twice the ownership level in other large US equities, mostly for their index broad market and REIT index offerings. StateStreet recently created a new sector fund just for real estate, XLRE. Expense ratios for REIT ETFs range from 0.07% for Schwab’s (SCHH) to 0.43% for iShares (IYR).

- Size of US commercial real estate market according to this study was $10T in 2009, which I assume has grown to $12T today. Size of REIT market cap and leverage ratio from REIT.com. REIT market ownership from 1991 based on the rate of growth of market cap of REITs being 22% and the NAREIT REIT price index growing at 4.7% pa over the period.

- Further assumptions are 5% initial property yield, growing 2% a year, and leverage of 50% at a rate of 4%.

- For this calculation, I assumed 5% lower tax rates and that 33% of management expenses are non-deductible for the private investor.

- Investing through a REIT ETF such as IDUP LN can eliminate capital gains tax, reduce the income tax rate by over half to 15% and eliminate the drag of non-deductible miscellaneous itemized deductions. This should not be taken as tax advice.

- “The Cost of Illiquidity” (see page 27 in particular).